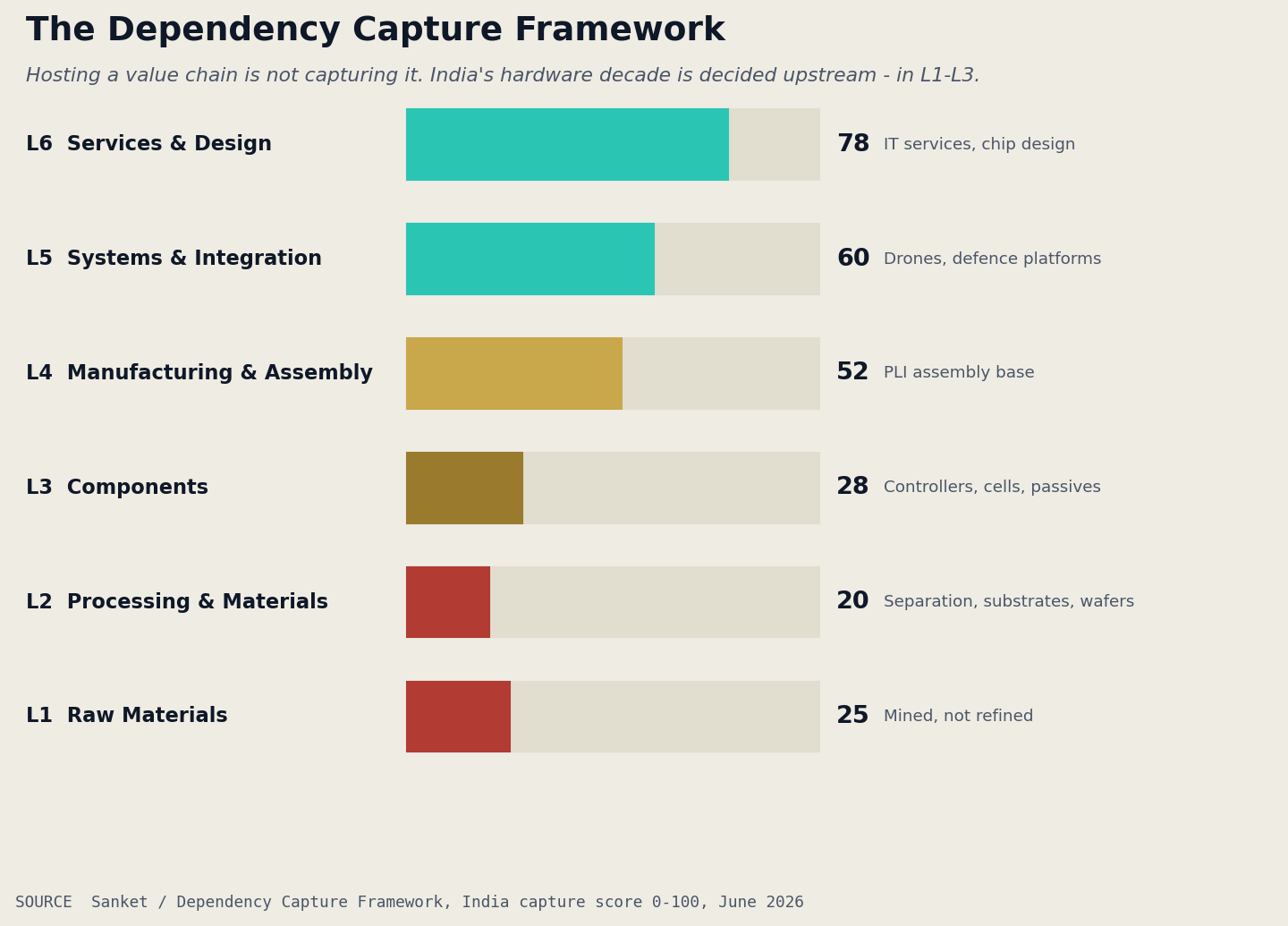

Assembly Is Not Sovereignty

Nine reports this month, one structural finding: India assembles — but the value lives upstream, in the layers it does not own. From the parts inside its drones to the software it runs on.

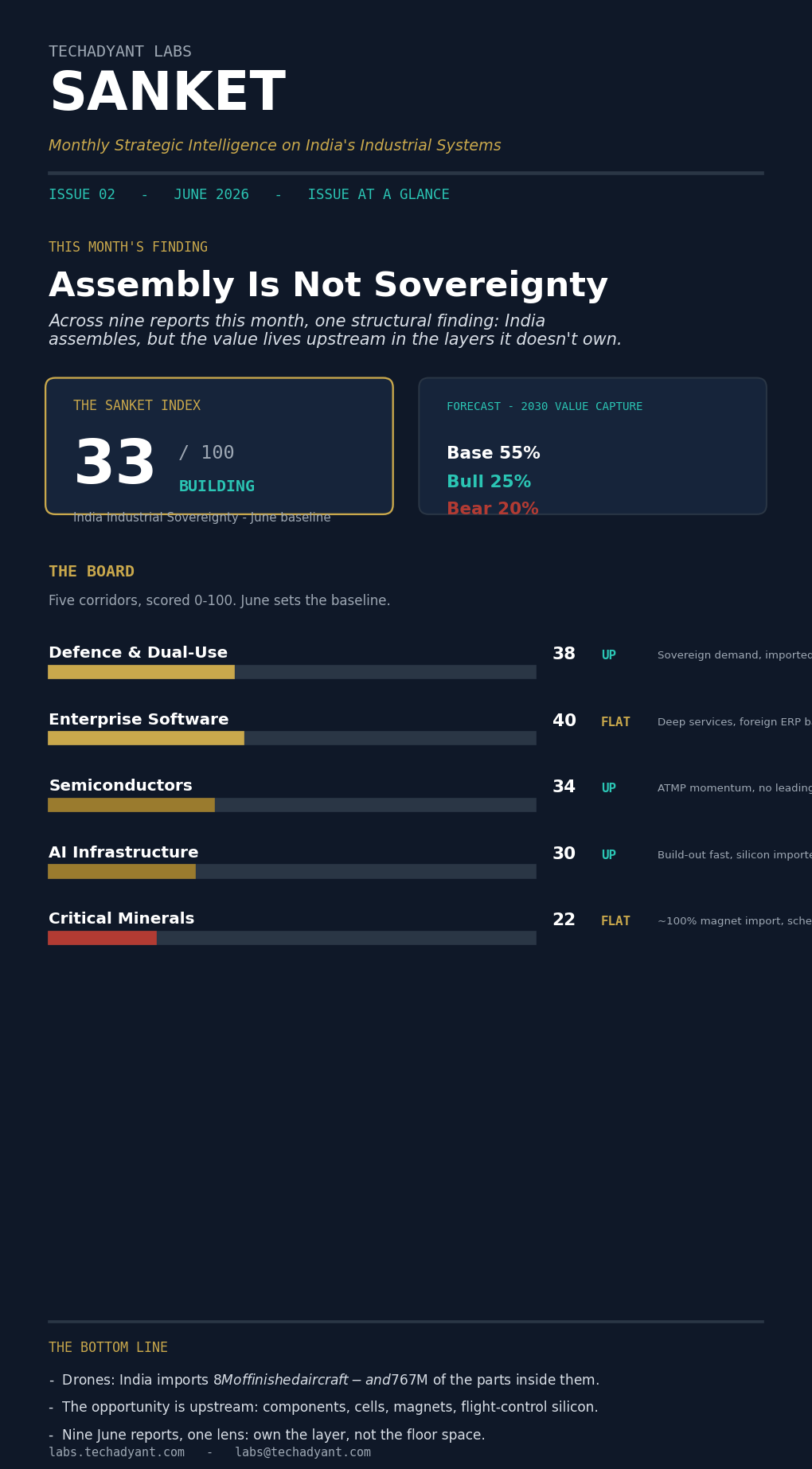

The issue at a glance

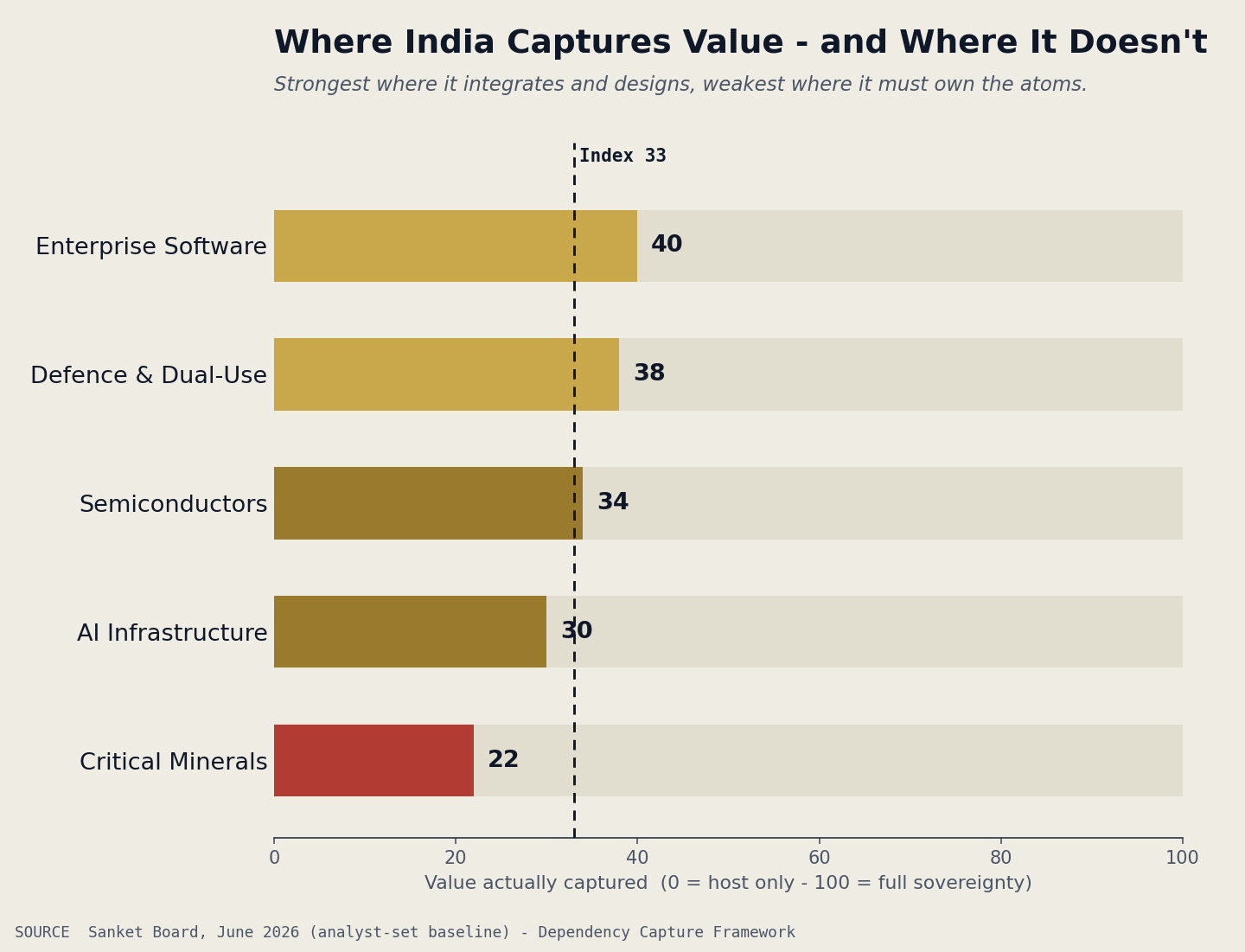

Five Corridors, Scored

India’s industrial sovereignty, read corridor by corridor on the Dependency Capture Framework™ — how much of the value India captures, not how much it hosts. June sets the baseline; from Issue 03 each reading carries its month-over-month move.

- One finding ran through all nine of this month’s reports: India assembles — the value lives offshore, in the components it imports.

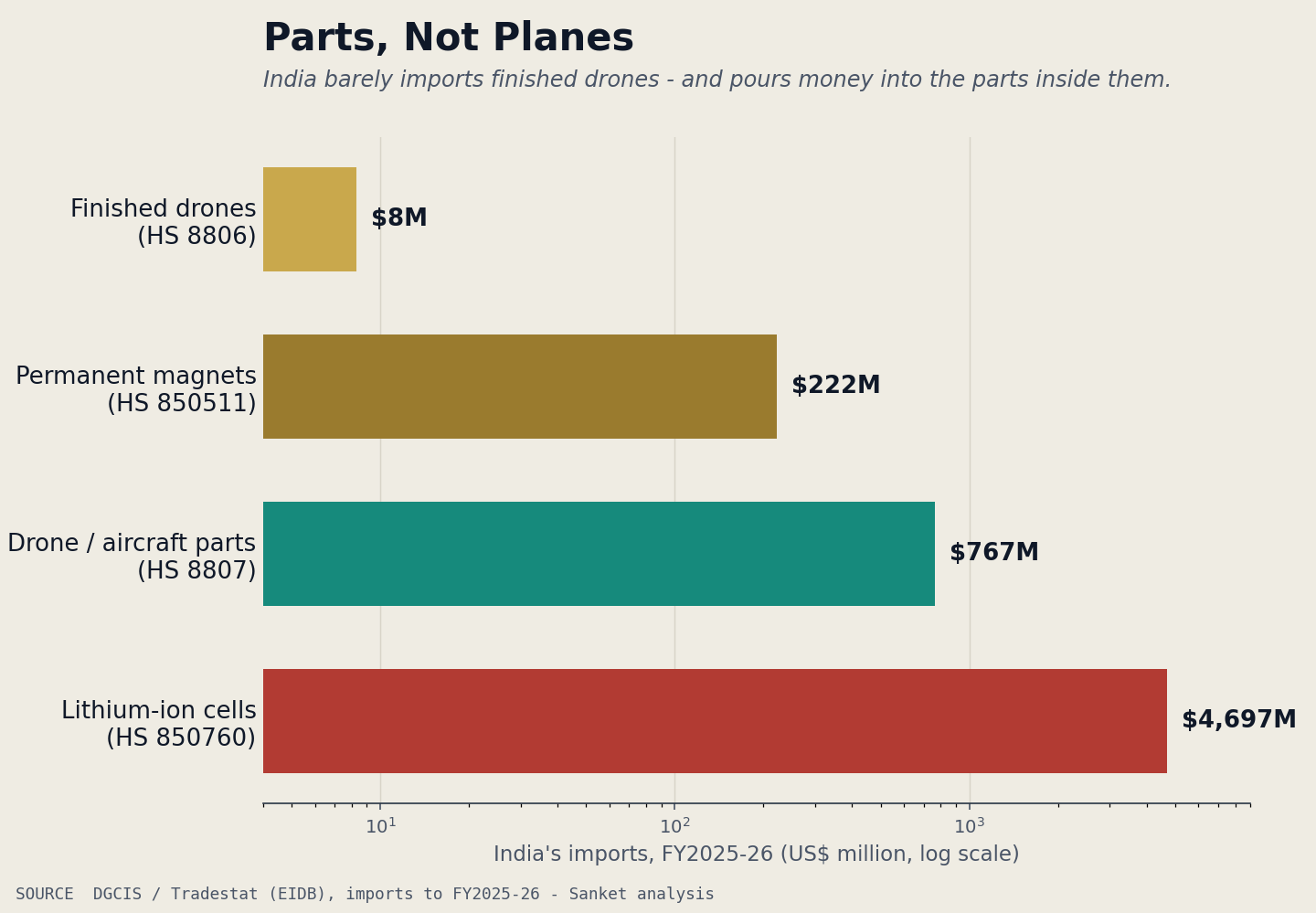

- Drones make it literal: India imported $8M of finished drones last year — and $767M of the parts inside them, plus $4.7bn of cells.

- The same pattern runs through software (foreign ERP), AI infrastructure (imported silicon) and minerals (imported magnets).

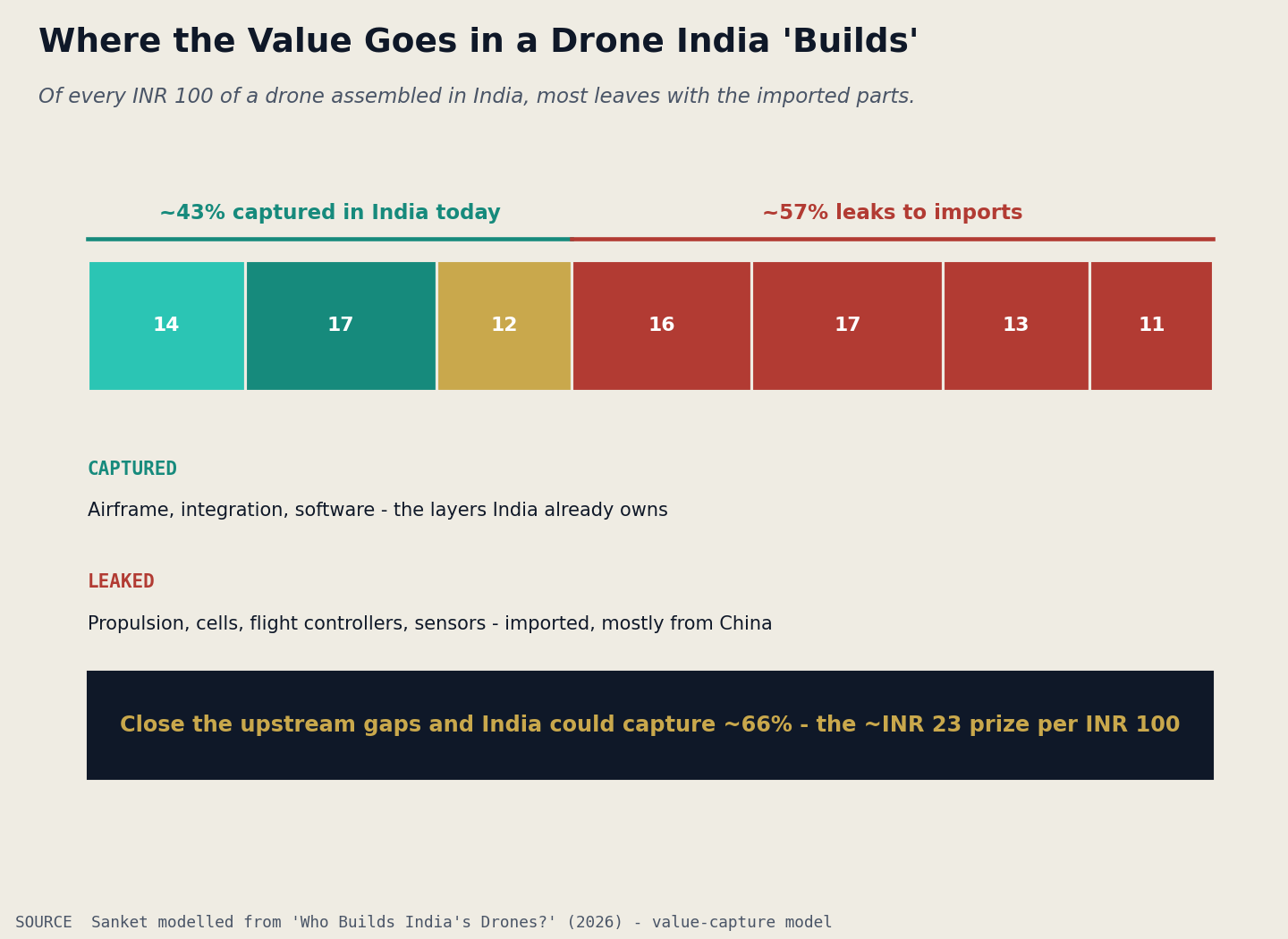

- The opening is upstream and ownable — components, packaging, cells, magnets, flight-control silicon — where ~₹23 of every ₹100 currently leaks abroad.

- Policy finally aimed there in June — ISM 2.0, the rare-earth magnet scheme, mineral corridors — but output, not announcements, is the test.

Assembly Is Not Sovereignty

For a decade India’s industrial story was told in headline numbers — plants opened, PLI disbursed, assembly lines lit. This month, across nine Techadyant reports spanning drones, semiconductors, enterprise software and AI infrastructure, the same structural fact kept surfacing: hosting a value chain is not the same as capturing it.

Drones are the clearest proof. India has built a credible integration and operations layer — it assembles, flies and fields drones at scale. But the motors, cells, flight controllers and sensors are imported. Customs settles the argument: $8M of finished drones came in last year against $767M of parts. India buys the parts, not the planes.

The pattern repeats by corridor. In enterprise software the country runs on foreign ERP it does not control; in AI infrastructure it is racing to host data centres on silicon it does not make; in critical minerals it mines what it cannot yet refine. Each is a different layer of the same dependency.

The opening is upstream, and it is real. The value India fails to capture — components, processing, cells, magnets, design-to-silicon — is exactly where June’s policy moved: ISM 2.0, the rare-earth magnet scheme, dedicated mineral corridors. The window is measured in quarters. The test is whether the value-add line moves — not whether more ribbons are cut.

Parts, Not Planes

The trade data is the thesis: the value India is missing sits one layer up — in the components, cells and silicon it buys instead of builds.

What Actually Moved in June

The month’s hard moves — capital, policy and capacity — tagged by corridor and sourced.

India’s Chip Startups Cross Into Production — on a Supply Chain They Don’t Control

Indian semiconductor startups are moving from prototype to commercial production on government incentives — a genuine step up the stack. But the wafers, tools and packaging they depend on remain China- and Taiwan-controlled. It is the thesis in miniature: India can design and build, while the atoms underneath stay foreign.

The tell to watch: whether a domestic supplier base forms around these firms — or whether India’s chip startups become design houses dependent on imported inputs and offshore capacity.

The ₹7,280 cr rare-earth magnet scheme funds 6,000 MTPA of capacity, with first production targeted by end-2026. India is finally backing the processing chokepoint, not the ore. The risk: a capacity gap before any line produces.

ONDC raises ₹220 cr from Zoho, Uber, Paytm and BSE — strategic, not financial, investors backing an open-network alternative to platform gatekeepers. The signal: India is building digital-commerce infrastructure it can govern.

China tightens outbound investment and tech-export rules, requiring authorisation to ship restricted goods, technology and data. Every Indian supply chain that routes through China just got riskier — and the case for upstream localisation stronger.

We assess that India’s binding constraint across all five corridors in 2026 is not demand or assembly capacity but upstream capture — components, processing and materials. June’s policy moves (ISM 2.0, the magnet scheme, mineral corridors) are correctly aimed at that layer.

Principal risk: the familiar one — incentives pooling in assembly while the hard inputs stay imported. Confidence is capped by India’s execution record on value-addition targets and by an 18–30 month lag before any new upstream capacity produces.

Where the Value Goes

The Dependency Capture Framework™

“India doesn’t lack factories. It lacks the layer underneath them.”

Nine Reports, One Lens

June’s research, each in a line and a number — the evidence behind this month’s thesis.

- India’s Unmanned Warfare Transformation — the Army’s UAS and loitering-munition roadmap to 2035, and the ~₹40,000 cr subsystem prize beneath the airframe.

- Who Builds India’s Drones? — $767M of parts vs $8M of finished drones.

- India’s Drone Propulsion Opportunity — a ~$1bn motor, ESC and jet-propulsion market by 2036.

- India’s Drone Battery Ecosystem — the cell-not-pack gap: ~60GWh pack vs ~1GWh cell.

- Who Controls India’s Drones? — ~90% of small-drone flight controllers imported.

- India Drone Sensors, Payloads & Imaging — the most import-bound layer of all, sized to 2035.

- The Opportunity Beyond the Fab — 100 startup and MSME opportunities, scored and ranked.

- The SAP Question — who really controls the enterprise software India runs on (free).

- The End of the Application Era — who captures computing when the application disappears (free).

“Make in India” Is Working — That’s the Problem

Consensus reads record assembly and PLI disbursal as success. We’d be careful. Assembly that imports its hard inputs is activity, not capability: it books revenue while the margin and the dependency stay offshore — which is precisely what the drone trade data shows.

The metric that matters isn’t units made or plants opened; it’s domestic value-add per unit and whether India owns the chokepoints. Cheer the factories. Stay sceptical until the value-add line actually moves.

Three Ways This Plays Out

India captures meaningful upstream share in packaging, cells or magnets, but stays dependent on imported tools and materials. Value up, ceiling visible.

The new schemes seed real supplier clusters; India crosses into chokepoint ownership in at least one corridor — magnets or advanced packaging.

Incentives fund assembly again; capacity scales but value leaks — Make-in-India 1.0 repeated one layer up. Floor space, not chokepoints.

Own the layer, not the floor space. The full June catalogue:

- Browse all reports →

- Forthcoming: The Packaging Frontier — OSAT and advanced packaging, the deep-dive behind this month’s framework.

- Commission bespoke research or a DPR → labs.techadyant.com/services

Get Sanket first

Monthly strategic intelligence on India’s industrial systems — independent and infrequent.