India Buys Into the Middle of the Stack

A $3.3bn substrate plant, a $150bn target, and a PLI that finally bites. May was the month India stopped chasing the fab — and started claiming the one layer it can actually own.

The issue at a glance

- The AI build-out stopped being a chip race in May — it became a capital, geography and defence story at once.

- India’s real opening is not the leading-edge fab. It is substrates, advanced packaging and components — and policy and capital both moved there this month.

- Three reinforcing moves: a $3.3bn Odisha substrate plant, NITI’s $120–150bn 2035 target, and PLI 2.0’s 55% domestic-value rule.

- Compute is being financialised — Apollo/Blackstone’s $36bn TPU lease-back turns a demand wobble into a credit risk.

- Defence supply chains are cracking open (US munitions gap to 2031) — an opening India can supply into, if it is ready.

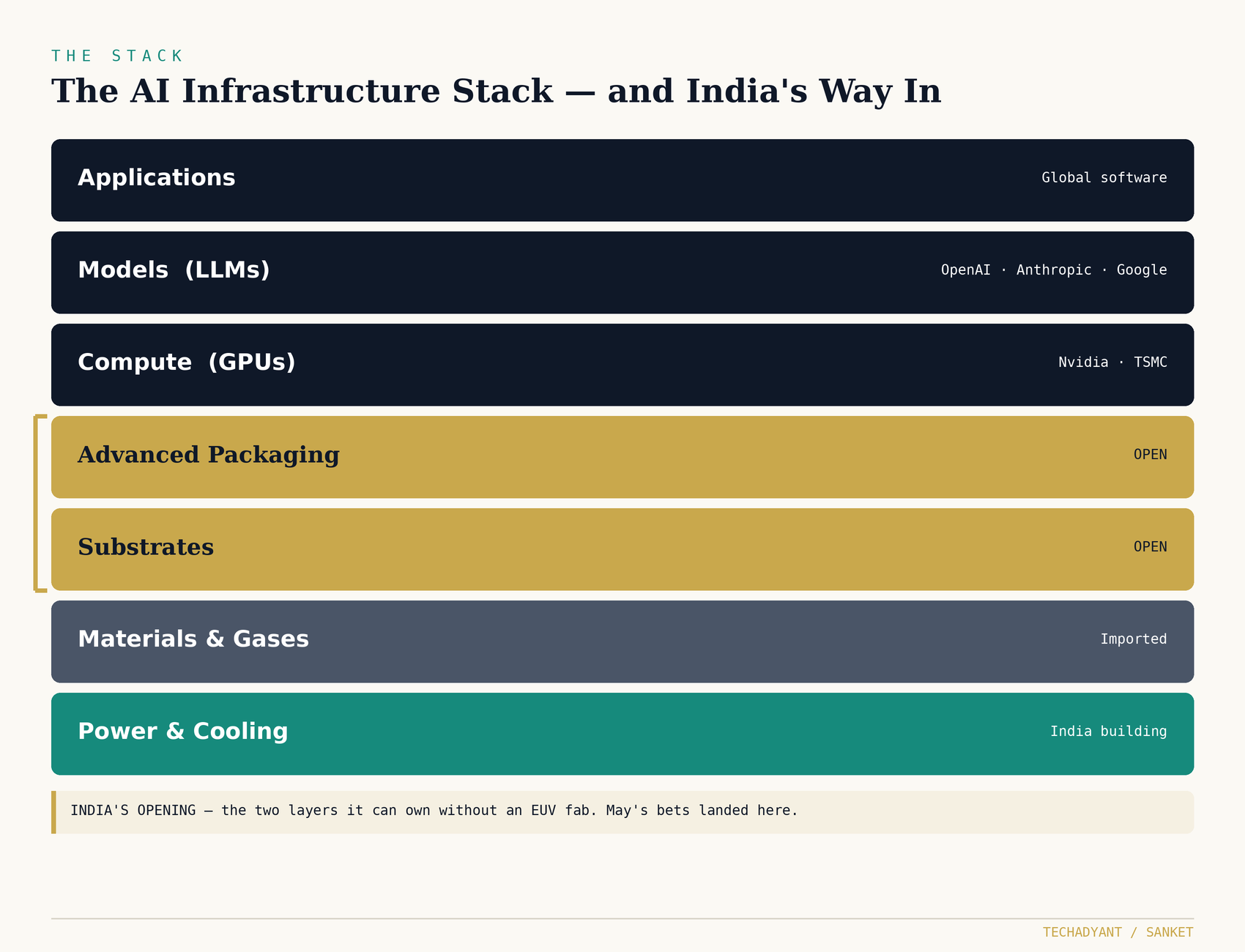

Win the Middle, Not the Edge

For two years, the AI story was a GPU story. In May it became something larger. Capital reorganised around it — Apollo and Blackstone’s $36bn. Geography reorganised — France, Brazil, a post-fab Europe. Defence reorganised — a US munitions gap that now runs to 2031.

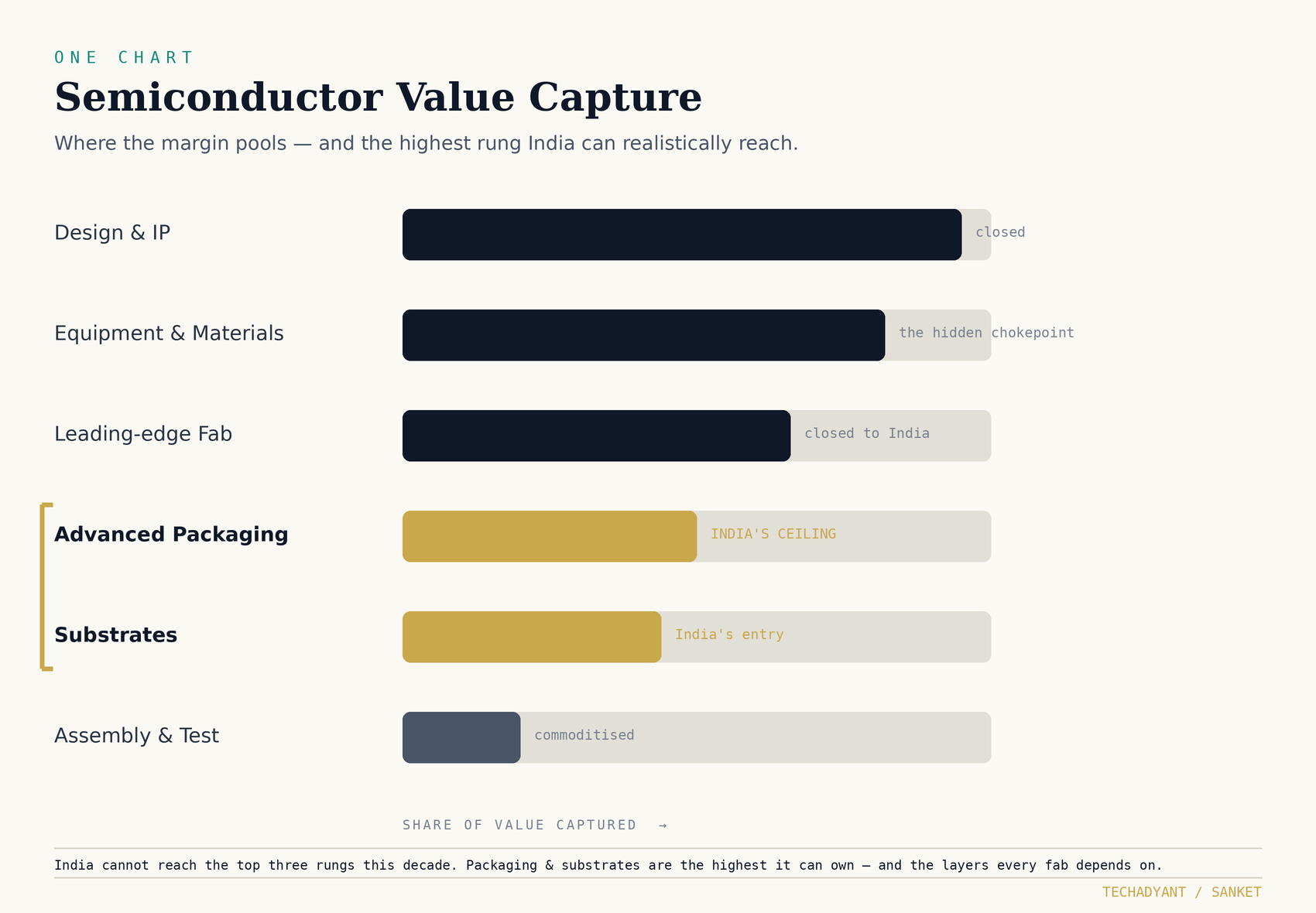

India cannot win the leading edge. That race belongs to Taiwan and Nvidia, and the entry ticket is an EUV fab India will not build this decade. But the stack has a soft middle: substrates, advanced packaging, components. Lower-glamour, lower-headline — and ownable.

This month, the Indian state and India-bound capital moved into that middle at once: Odisha, the NITI target, PLI 2.0. The window to claim it is measured in quarters, not years.

Semiconductor Value Capture

The top three rungs are closed to India this decade. Advanced packaging and substrates are the highest it can own — and the layers every fab depends on. That is the whole bet.

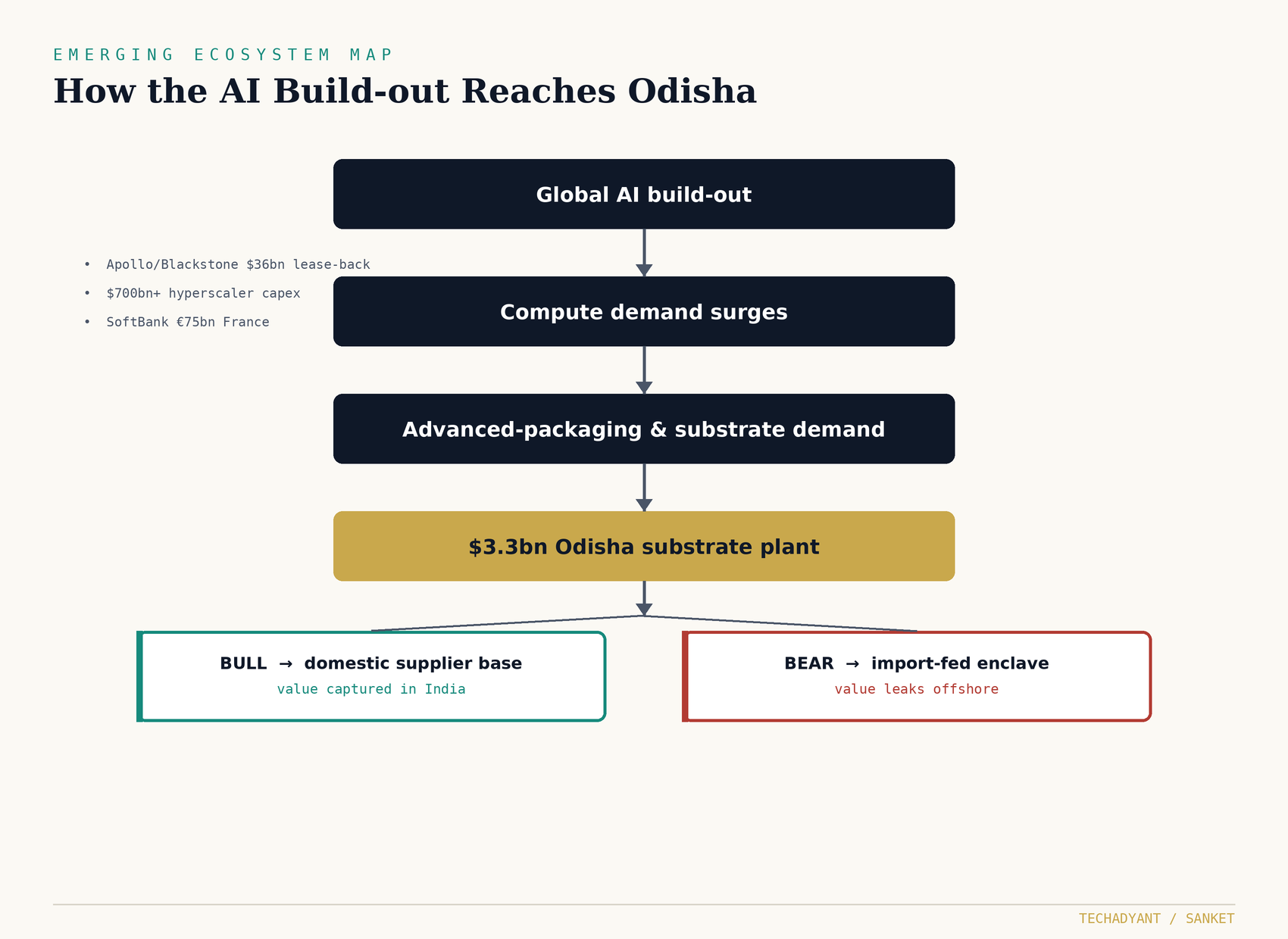

$3.3 Billion Lands in Odisha — and It’s Substrates, Not Silicon

Intel and 3DGS will build an advanced-packaging substrate plant in Odisha. Substrates are the quiet chokepoint of the chip world — the layer you can own without an EUV fab, and the one Western and Chinese supply chains are now scrambling to secure. The first time India’s “package, don’t fabricate” logic shows up as poured concrete, not commentary.

The tell to watch: whether a domestic substrate supply base forms around the plant — or whether it becomes an import-fed enclave that books its value offshore.

NITI Aayog sets a $120–150bn semiconductor value-chain target to 2035, with the state funding a third to de-risk it. A co-investment model is how Taiwan and Korea were built. The signal: India will underwrite, not wait.

The new mobile-phone PLI mandates over 55% domestic value addition. PLI 1 made India an assembler; PLI 2 targets the component base beneath it. The risk to watch is paper compliance over real localisation.

Apollo and Blackstone structure a $36bn lease-back so Anthropic can buy Google TPUs. Compute is now financed like real estate — which means the next demand wobble is a credit event, not just a tech story.

We assess that India’s most defensible semiconductor position through 2030 is advanced packaging and substrates — not fabrication. May’s three commitments are mutually reinforcing, not coincidental: target, capital and incentive now point at the same layer.

Principal risk: enclave economics — incentives concentrating in assembly that imports the hard inputs, leaving the value and the dependency offshore. Confidence is capped by India’s execution record on PLI value-addition targets.

How the AI Build-out Reaches Odisha

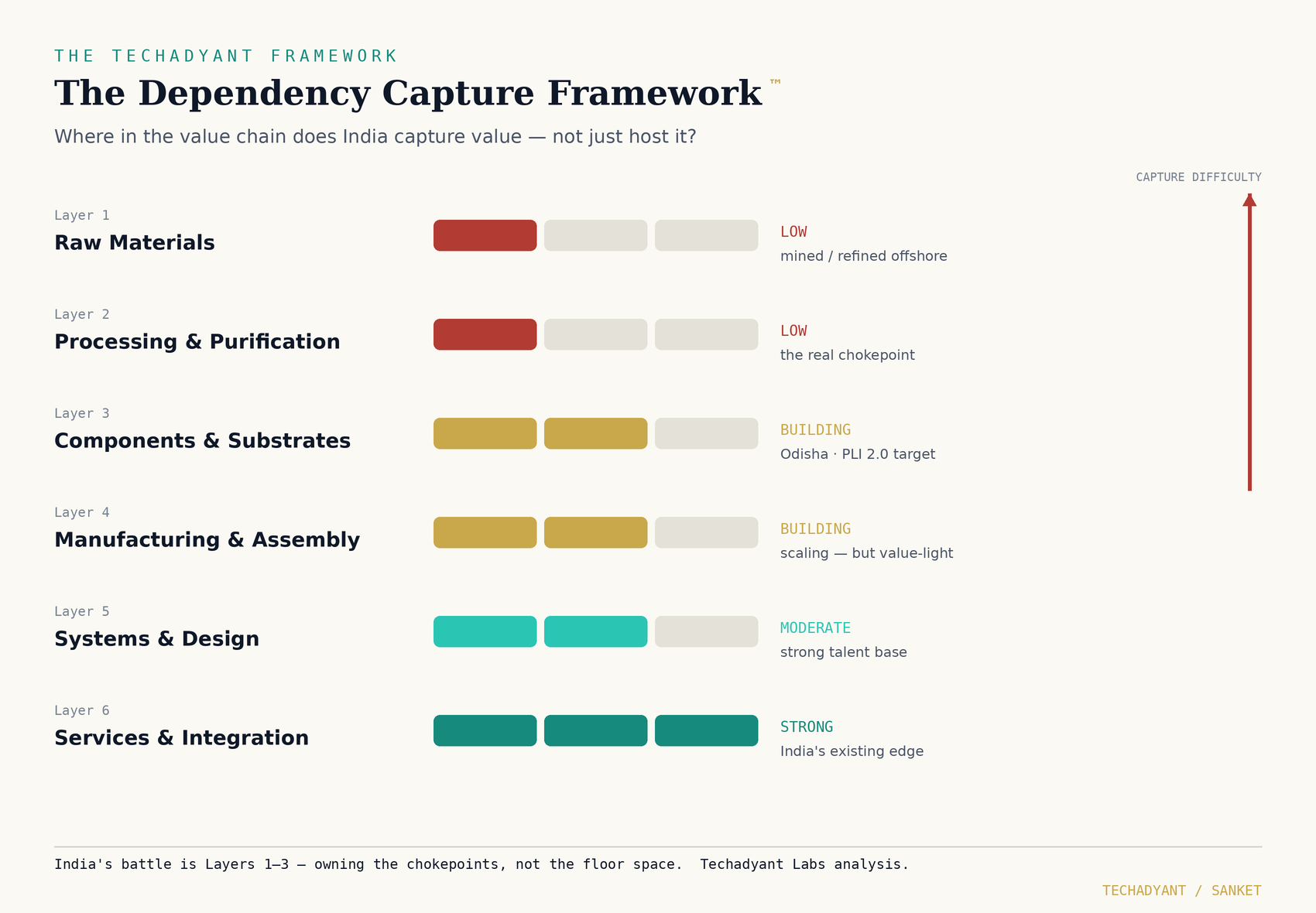

The Dependency Capture Framework™

“India doesn’t need an EUV fab to win. It needs to own the layers every EUV fab depends on.”

The $150 Billion Number Is the Wrong Target

Consensus cheered NITI’s $120–150bn goal. We’d be careful. Headline value-chain size is a vanity metric: a country can host $150bn of assembly and capture almost none of the margin — which is precisely what the first PLI delivered.

The number that decides India’s hardware decade isn’t chain size; it’s domestic value-add per dollar, and whether India owns the chokepoints — substrates, materials, equipment subcomponents — or merely the floor space they sit on.

Three Ways This Plays Out

India secures meaningful share in advanced packaging and substrates, but stays dependent on imported materials and equipment. Value captured, ceiling visible.

A domestic supplier ecosystem forms around Odisha — India’s first globally competitive semiconductor cluster, capturing value up the chain.

Packaging scales but stays import-dependent — a repeat of PLI 1.0’s assembly-heavy, value-light outcome. Floor space, not chokepoints.

The full report behind this month’s thesis publishes 15 June: The Packaging Frontier. Related reading from the Labs:

- Who Really Benefits from India’s Fab Ecosystem?

- India’s AI Industrial Transition (2026–2035) — free

- Commission bespoke research or a DPR → labs.techadyant.com/services

Get Sanket first

Monthly strategic intelligence on India’s industrial systems — independent and infrequent.